Wealth Management Guiding Principles

Guiding principles can form an operating philosophy that can help guide you throughout your working and investing life in all circumstances, irrespective of changes in your goals and objectives.

Contact Us

We specialize in helping individual investors just like you accomplish their financial and life goals. We bring breadth and depth-of-field, discipline and energy to your planning effort. Once we have helped you develop plans intended to help you accumulate enough investment assets to achieve the financial and other goals you have, we build and manage your investment portfolio to help you meet your needs.

To learn more about how we may be able to help you, please call us at (480) 951-2900.

The Importance of Guiding Principles.

Guiding principles help keep us on a commonsense path for our unknowable financial life journey. We can glean these helpful principles from those who have successfully gone before us. As we study the success of others, we can learn from their success. Their success has come from experience, and their experience has come from their mistakes.

Investor mistakes are generally expensive, so studying success has the advantage of reducing the “tuition costs” of our learning.

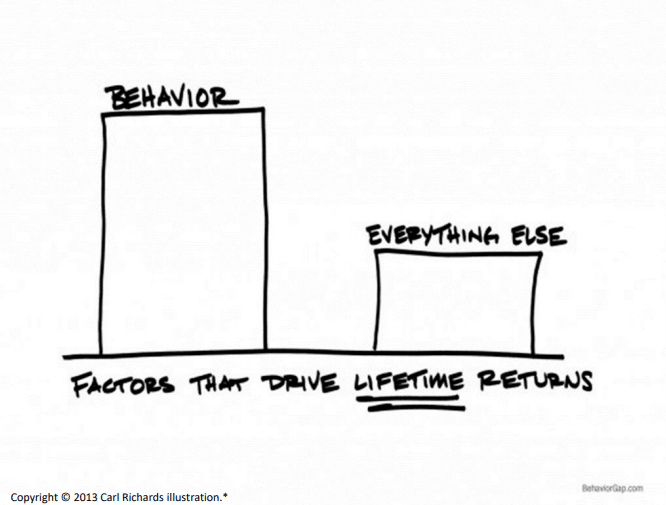

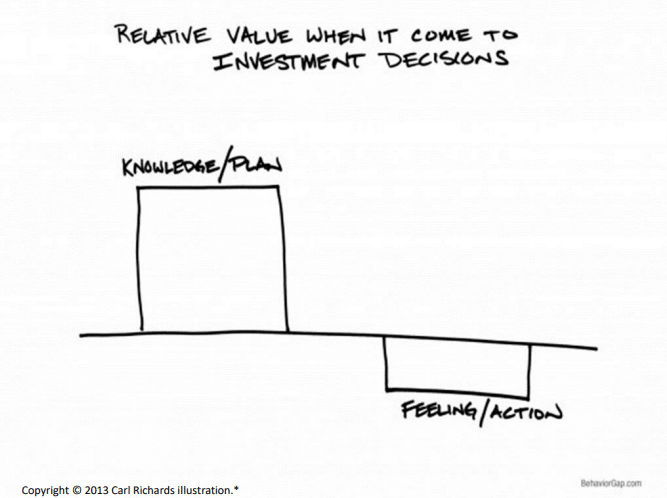

Your investing behavior may have the largest impact on the long-term results of your investment returns and your success or failure in meeting your financial needs.1

Bright minds have advanced compelling arguments for both passive index investing and active investment management. If the argument for low-cost indexing holds appeal for you (i.e., lower costs result in higher investor returns), you still must tackle the thorny observation and risk that you may fail to achieve market-index returns.

Key Learning

The cause of this costly difference is investor behavior, dubbed the “Behavior Gap.” The behavior gap is the amount by which your personal investment performance may underperform the actual returns of your investments. It is caused by emotionally untimely decisions to change funds, change advisors or buy and sell securities in your accounts.

1. Your Vision is Your Responsibility.

It may seem obvious, but you are solely responsible for developing a clear idea of what you want to accomplish and how you will use your money to support your goals. For those who ignore or procrastinate addressing this responsibility, the risks of missteps and bad outcomes are high.

Key Learning

Let’s start with why you are investing. It’s simple, but may not be obvious. You are investing because at some point in the future, you will need income. It may be as soon as tomorrow or it could be years in the future. When you stop to think about it, if you’ll never need an income, you don’t need to

invest. Precious few of us, however, were born into circumstances in which we will never need an income.

So your investing is simply driven by your need for an income now, an income in the future, or both. The income you need may be for a moment in time (a one-time purchase) or through a period of time (a retirement income).

Takeaway

You will be well-served to determine the amount and timing of your need for income. Measuring the amount and timing of your income needs will better inform the types of investments and strategies you will need and the types and amounts of risk you will need to endure to meet your needs. Having a vision for what you want and a plan to achieve it will help reduce unwise choices and the resulting costs of the behavior gap.

2. Save. Then Save More. You Will Need Savings.

Your investing cannot begin or be sustained unless you have money to invest, so begin by developing the discipline to save. You will need to either save and hold onto money you’ve inherited or you’ll need to save some of the money you earn, or possibly both. Some of us will be fortunate enough to inherit, but most of us will need to save some of the money we’ve earned and invest it for the day when we are no longer able to work or wish to stop working.

Key Learning

It’s important to remember that if you are an inheritor, you may have really inherited about twice as much as the value of your inheritance because it may have taken as much as $2.00 in pre-tax earnings to pass along every after-tax $1.00 you received. If you are accumulating your savings for

investment from your after-tax earnings, the story is the same. You have to earn more than $1.00 pre-tax for every $1.00 of after-tax savings.

3. Pay Yourself First.

Key Learning

We are at the beginning of the next great crisis we will face in this country: households undersaved for retirement. One of the primary reasons households are undersaved is the difficulty of trying to save after all of the bills have been paid. Instead of attempting to save what’s left after the bills

are paid (which is usually not enough), put your savings away first and adjust your lifestyle to live on what’s left.

4. Protect Your Capital.

Once we are reminded of our true cost of our after-tax savings, we can better appreciate the first rule of successful investors. “Don’t lose the money.” Investing, like so many other aspects of life, isn’t so terribly difficult. What makes it difficult is recovering from the mistakes we make.

Protect Your Capital, Revisited.

Key Learning

The second rule of successful investors? “Don’t forget Rule #1.” The second rule isn’t meant to be trite or to trivialize the first rule. It is meant to remind us that we only have so much vitality to suffer losses of our capital and work more to replace the lost savings, and that not every day is filled with

serendipitous opportunity.

Takeaway

What does “Don’t lose the money,” really mean? We believe it means to invest, not speculate. Invest with prudence, discretion and intelligence. Invest your capital for the long term and consider the probable income, as well as the probable safety of the capital you invest.

Takeaway

The admonition to not “lose the money” doesn’t mean don’t take risk. It means to embrace risk in a thoughtful and intelligent manner that minimizes the risk of large losses – wipeout risk – and positions you for the opportunity to earn a worthwhile reward for the risks you take.

The financial rewards of successful investing attract the brightest and sharpest minds. Successful investors approach their investing endeavors with a humility and respect for the competitive strength of the field.

Anyone with meaningful investing experience has had the experience of being parted from their money. It doesn’t feel good.

For those with the determination to carry on, they begin to ask themselves, “What is it that I don’t know that I don’t know.” Put differently, they learn to use their prior experiences of insufficient inquiry and prudence as a reminder to be more circumspect and disciplined the next time they commit their precious capital.

5. Look for Consistent Cash Flow.

Key Learning

Once they understand that return of their capital has priority over return on their capital, successful investors begin their endeavors to seek profitable investments. They understand that investment opportunities that do not generate regular cash flows are really speculations about future price increases of the asset they are considering for purchase. They also recognize that investment opportunities that do not generate regular cash flows are also more risky than investment opportunities with regular cash flows.

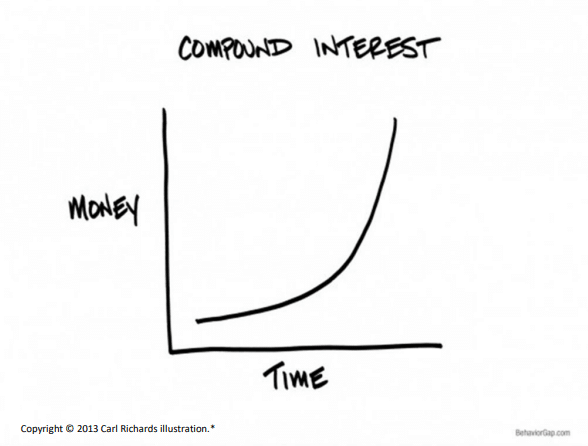

6. Understand the Power of Compounding Your Returns.

Depending on the source, urban legend has it that Albert Einstein referred to compound interest as “the eighth wonder of the world, the human race’s greatest invention, or the most powerful force of the universe.”

To absorb the astounding power of compounding, imagine your job is to contact the 2.2 million plus employees of Walmart by telephone in an emergency situation. You have two choices to get the job done.

You can make all of the calls yourself, averaging one minute per call. Assuming you reach everyone on the first try, you will have completed your job after calling for more than 1,527 days ─ more than four years, working 24 hours a day, seven days a week!

Or, every time you completed a call, you could ask the person you called to join you and keep calling with you. And you could ask the next two people each of you called to join you and keep calling with you. And so on, and so on. The time to complete the job of calling all 2.2 million employees would be reduced from more than four years to approximately 22 minutes. Now that is astounding compounding power!

Key Learning

So, compound growth represents the growth on growth over time, with the increase for each time period added to the original value before growing again in the next time period. Now, re-imagine this exercise with money. Instead of spending the interest you receive from your bonds or the dividends you receive from your stocks, you reinvest that cash and buy more bonds and stocks, which generate yet more interest and dividends.2

As you can see below, the growth does not occur in a straight-line fashion. It occurs in an upward-curving fashion because the amount of your money at work is increasing exponentially with each additional period.

Takeaway

Time and compounding can generate significant wealth for you if you save and reinvest your cash flow.

7. The Value of Money.

Money facilitates commerce and is supposed to provide a stable storehouse of value. The value of money is nothing more than what it will buy. Unfortunately, paper currency, especially U.S. paper currency, has a history of depreciating in value, failing to preserve its long-term purchasing power.3

Takeaway

This has implications for you as you consider how you will invest your precious savings. If the value of your money erodes over time due to inflation, then preserving the purchasing power of your savings will need to be one of your objectives.

8. You Have Only Two Investment Choices.

Key Learning

There are only two investment choices you can make with your savings. You can either be an owner or a lender.4 If you loan your savings to someone else at interest, you will receive one promise to be paid interest on a timely basis and another promise to be repaid when the loan matures.

The advantage of loaning out your savings is that you can schedule the cash flows of interest and principal to meet your future needs. The potential disadvantage of loaning out your savings is that the repayments coming back to you in the future may be in dollars that won’t buy you as much because of any inflation that occurred since you loaned out your savings.

The advantage of owning assets ‒ a business, real estate, natural resources, commodities, royalties, etc., ‒ is that your future cash flows of earnings, dividends, rents or sales proceeds may increase during inflationary periods. Any increased future payments you receive will help to offset any purchasing-power loss you suffer while waiting for those payments.

The potential disadvantage of being an owner is that there are generally no contractual guarantees of future cash flows or repayment of your capital, meaning the cash flows to you are questionable and lumpy, not predictable.

As a general rule, knowing the timing and amounts of your cash flows (predictability) helps you sleep well at night, while the prospect of receiving increasing cash flows (greater abundance) brings you comfort that you will likely continue to eat well.

The tradeoff for investors, then, is sleeping well versus eating well. Historically, the more predictable long-term “sleep-well” returns from loans have been lower than the more abundant long-term “eat-well” returns of owners.

This makes sense for two reasons. First, interest payments and capital repayments from loans are more predictable than distributions to owners after all other expenses have been paid. Owners only earn their returns after the lenders have received theirs.

Lenders have a priority claim over owners on cash flows. Owners should expect to earn more than lenders because their returns are less certain and they stand second in line to receive the earnings that remain after the lenders have been paid.

Takeaway

So, the general rule is that long-term owners earn more than long-term lenders. We know this must be true over the long haul or owners would not get out of bed in the morning and go to work if they didn’t have a reasonable chance of earning more than the costs of their borrowed capital. They would just stay home and resign themselves to being long-term lenders of capital.5

9. Own Profitable, Growing Businesses for a Long Time.

Now that we’ve covered the necessity of saving, the power of compounding and the larger long-term returns available to owners, let’s focus on how you can combine saving, compounding and ownership to increase the cash flows you receive for saving and reinvestment.

It’s easy to sleep well at night if you have no debt and enjoy a stream of rising income. Owning profitable, growing businesses improves your probability of enjoying those outcomes and time does the work.

Academic studies reveal that a well-diversified portfolio of stocks has been capable of producing 9% – 10% compound annual returns over the long run. 6 Here then, is a key question: Are you, or will you be, a long-term owner of profitable growing businesses? We know that this is a key question, because other empirical studies reveal the risk that an average mutual fund investor may have captured only 3-4% of the long-term 9-10% returns that stocks have offered.

Key Learning

Where does the other 5-7% missing return go? The return slips away due to the short-term behavior of trading (buying and selling) in stocks as opposed to the long-term behavior of owning (holding) the underlying businesses. This speculative trading intensifies when people fear they are missing an

opportunity to make money when the market goes up (greed) and when people fear they are going to lose money when the market goes down.

Trading stocks, versus owning profitable, growing businesses for a long time, decreases the probability of successfully building rising streams of income.

10. Earn Worthwhile Rewards for the Risks You Take.

Imagine you and a friend walk into a casino to play roulette. You each have $1 million to bet. As you approach the roulette table, your friend says, “I’m thinking Black 33.” Astonished at the coincidence, you reply, “Me too!” Both of you, marveling at the odds of the coincidence, place your bets on Black 33. He is feeling very lucky and decides to bet all $1 million on Black

33. You are feeling lucky too, but decide to bet just $10,000 of your $1 million on Black 33 as well.

Question: Will the size of your friend’s bet (100 times larger than yours) improve the probability of the marble coming to rest on Black 33? No. The odds are the same for both of you no matter the size of your bets. Your friend is taking 100 times greater risk than you, without any opportunity to improve the probability for success. This is an unrewarded risk.

Key Learning

Successful investors try to avoid or minimize unrewarded risks and intelligently diversify the risks they take for worthwhile rewards.

11. Diversify Intelligently.

Successful investors not only allocate their investment capital to risks for which there is the opportunity for a worthwhile reward, they also allocate their capital to avoid the risk of taking large losses ‒ wipeout risk.

They do this by diversifying sources of return, such as growth of corporate earnings and dividend payments from stocks, stated coupon payments from bonds and rents from real estate.

Takeaway

Successful investors endeavor to never lose sight of what, how and when things could go wrong, and by how much. They recognize the need to be future-focused and see beyond the moment.

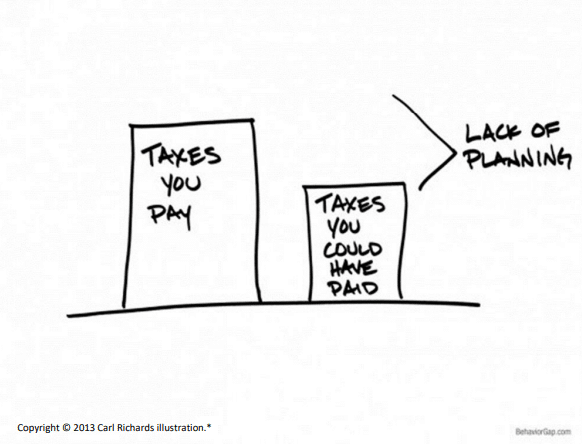

12. Plan Your Tax Exposure and Exit Strategy.

Key Learning

Before successful investors commit capital, they consider how to best hold title to the investment they will make and their exit strategy. These considerations help them in their efforts to minimize their tax exposures.

The number of tax regimes we are all faced with is mind-boggling. Trying to determine your marginal or effective tax rate ranges from highly unlikely to virtually impossible. Even your CPA isn’t likely to be able to figure it out without a computer and specialized tax software.

Successful investors understand the value of advance tax planning. They recognize that tax-planning opportunities occur at the beginning, not at the completion of an investment or tax year.

These represent just a few of the more significant tax exposures we all face and that you may need to consider in your tax planning:

- Federal Income Tax

- State Income Tax

- Local Income Tax

- Alternative Minimum Tax

- Capital Gains Tax

- Surtaxon Investment Income

- Social Security Tax

- Medicare Tax

- Corporate Income Tax

- Estate and Gift Tax

- Generation-Skipping TransferTax

Takeaway

While successful investors avail themselves of tax-planning opportunities, they do not let the tax tail wag the investment dog. They are also careful to engage in tax planning that is flexible enough to help them respond to changing market conditions, tax law changes and unexpected outcomes.

13. Build a Team of Knowledgeable Professional Advisors.

Key Learning

Successful investors know what they know and know what they don’t know. They have learned to be wary of unwittingly finding themselves in the position of not knowing that they don’t know.

While the world of financial services has evolved to provide investors with broad access to low-cost investment products and discount commission trading, successful investors recognize the value of knowledgeable and experienced financial, accounting and legal professionals. They learn not to overpay for their investments and they learn there is no substitute for the valuable knowledge and experience of competent counsel.

In the words of famous oilwell firefighter Red Adair,

Takeaway

“If you think it’s expensive to hire a professional to do the job, wait until you hire an amateur.”

A Closing Thought.

All of us have time, talent and treasure in different measure. Most of us begin life with time and no talent or treasure. As time passes, our talent and treasure grow, and the amount of time we have remaining decreases.

The best answers you seek to help you become a more successful investor are really the right questions to ask to help you enjoy a better life.

Thank you for sharing your time with us. We wish you continued success.

Footnotes.

1 Since 1994, Boston-based research firm DALBAR, Inc., has been measuring the effects of investor decisions to buy, sell and switch into and out of mutual funds over both short-term and long-term timeframes.

The results consistently show that the average mutual fund investor earns less, in many cases much less, than the long-term performance of the mutual fund itself. This often times results from a lack of planning and guidance.

The average equity mutual fund investor has underperformed the S&P 500 by at least 4% per year for all long-term investment periods since 1984. The original analysis began in 1984.

Source: DALBAR, Inc. 2012 Quantitative Analysis of Investor Behavior.

2 We explore compound returns in depth in our 2017 original research paper, Deliberate Dividend Growth Investing for Rising Income and Capital Growth.

3 See Michael F. Bryan, On the Origin and Evolution of the Word Inflation, Federal Reserve Bank of Cleveland, October 15, 1997.

4 At first, you may be thinking to yourself that this statement is too simplistic to be true and that there are many more investment choices than just being an owner or a lender. This is just a fundamental view from basic accounting principles and the standard balance sheet equation.

| Assets | = | Liabilities | + | Owner’s Equity | [formal equation] |

| Value of your stuff | = | Money you owe to lender(s) | + | Your equity after repaying what you owe | [less intimidating] |

| Investment | = | Lender | or | Owner | [investment choices] |

The two claims on an asset (investment choices) are ownership claims or lender claims. That’s how balance sheets are constructed.

Think about your house. If you own your house, don’t have any liens and you don’t have a mortgage loan, then the only legal claim to its value is yours, since you are financing its entire value with your money ‒ as an owner of capital.

However, if you have a mortgage loan, then there is an additional senior legal claim to its value [with priority to secure repayment], since you are financing some portion of its value with borrowed money provided by a lender of capital.

5 As a general rule, business owners only borrow capital to invest when they can identify investment opportunities offering returns higher than their cost of borrowed capital.

6 See Ibbotson® SBBI® Classic Yearbook 2013.

Disclaimers.

This paper has been prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any securities, or to participate in any trading strategy.

We believe the information we’ve presented in this paper is factual and up-to-date, but we do not guarantee its accuracy and you should not regard this paper as a complete and exhaustive analysis of the subjects we’ve discussed. All of the opinions we’ve expressed reflect our judgment as of the date we published this paper and are subject to change.

You should not construe the content of this paper as being personalized investment advice. You should engage a professional advisor before pursuing any of the investment ideas or implementing any of the strategies we’ve

presented in this paper.

ICW Investment Advisors LLC, doing business as Intelligent Capitalworks, is registered as an investment adviser with the Securities and Exchange Commission (SEC) and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission, nor does it indicate that the firm has attained a particular level of skill or ability.

Past performance may not be indicative of future results. All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for your portfolio. There can be no assurances that an investment or portfolio will match or outperform any particular benchmark.

Working with a financial advisor is not a guarantee of future financial success.

Always consult an attorney or tax professional regarding your specific legal or tax situation. ICW Investment Advisors LLC does not provide legal, tax, accounting, actuarial, or pension consulting advice or services.

______________________________________________________________

* All illustrations are copyright-protected property of Carl Richards and are reproduced as licensed materials pursuant to a Digital Content License Agreement between ICW Investment Advisors LLC and Behavior Gap LLC.

Single-copy printing of this guide is permitted as an incidental PDF download from the Intelligent Capitalworks website. Volume printing of this guide is not permitted without written permission from ICW Investment Advisors.